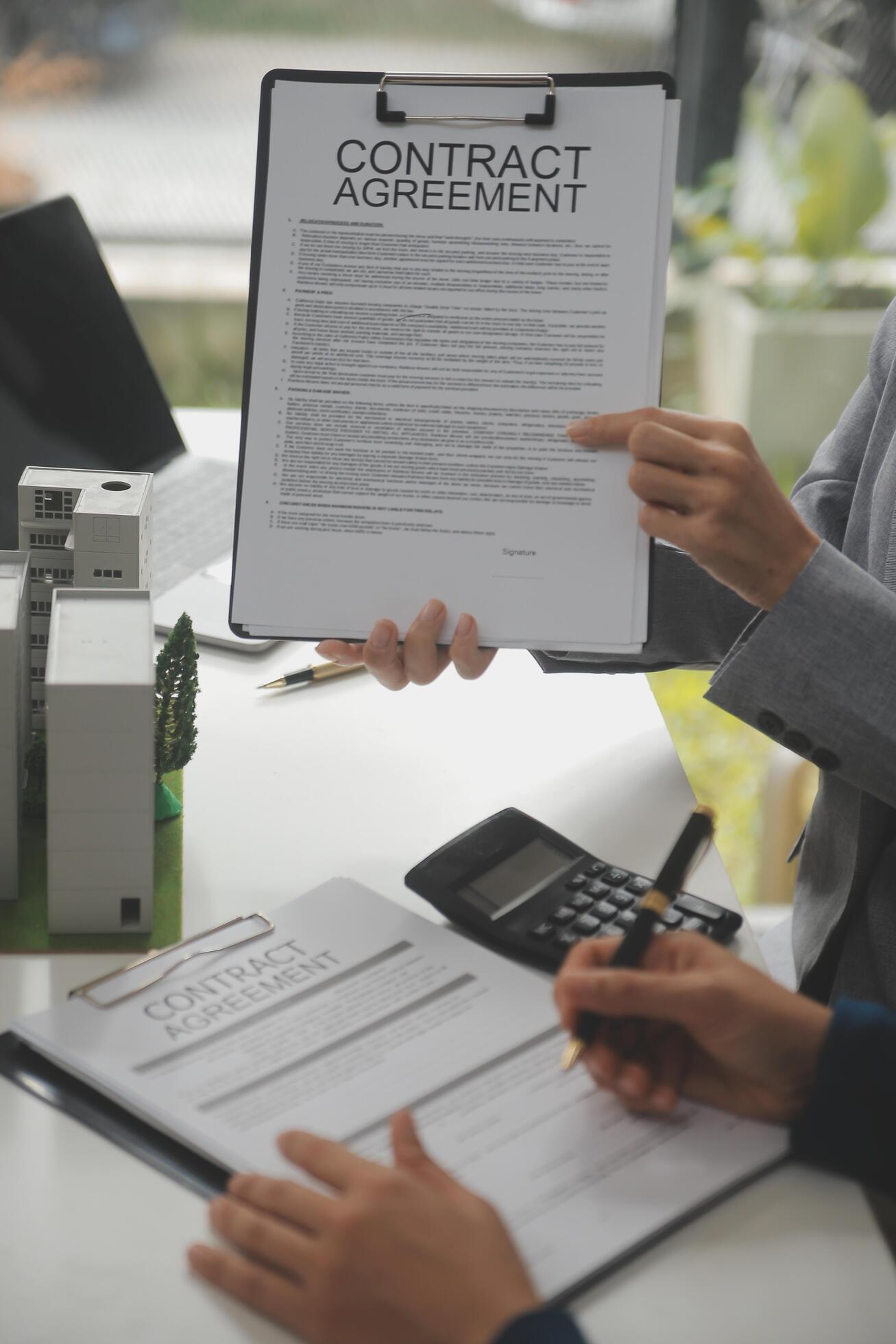

The world of real estate is a complex and ever-evolving landscape, with numerous factors influencing the buying and selling of properties. One of the most critical aspects of this process is the contract, which serves as a binding agreement between two parties. In the context of buying and selling a house, a contract is essential in outlining the terms and conditions of the transaction, ensuring a smooth and hassle-free process for all parties involved.

A contract in real estate typically includes details such as the purchase price, payment terms, closing date, and any contingencies that may arise during the transaction. It also outlines the responsibilities of both the buyer and the seller, including any repairs or maintenance that may be required. In the case of a home investment loan, the contract may also include provisions related to the loan terms, interest rates, and repayment schedules.

Insurance agents play a crucial role in the real estate process, particularly when it comes to home investment loans. They analyze the risks associated with the investment and provide guidance on the best course of action to mitigate those risks. This may involve recommending insurance policies that protect against unforeseen events such as natural disasters, theft, or damage to the property.

One of the key considerations for insurance agents when analyzing home investment loans is the potential for depreciation. As a property ages, its value may decrease, which can impact the loan’s value and the investor’s returns. Agents must carefully evaluate the property’s condition, location, and market trends to determine the likelihood of depreciation and recommend strategies to minimize its impact.

Another critical factor for insurance agents to consider is the loan-to-value (LTV) ratio. This ratio represents the percentage of the property’s value that is financed through the loan. A higher LTV ratio may increase the risk of default, as the borrower may struggle to make payments if the property’s value declines. Agents must carefully review the loan terms and ensure that the LTV ratio is reasonable and manageable for the borrower.

In addition to analyzing the loan terms, insurance agents must also consider the borrower’s creditworthiness and financial situation. A borrower with a poor credit history or unstable income may be at a higher risk of default, which can impact the loan’s value and the investor’s returns. Agents must carefully evaluate the borrower’s financial situation and recommend strategies to mitigate any risks associated with the loan.

The role of insurance agents in the real estate process is multifaceted and requires a deep understanding of the complex factors involved in home investment loans. By analyzing the risks and opportunities associated with these loans, agents can provide valuable guidance to borrowers and investors, helping them make informed decisions that minimize risk and maximize returns.

In conclusion, the contract is a critical component of the real estate process, outlining the terms and conditions of the transaction and ensuring a smooth and hassle-free process for all parties involved. Insurance agents play a vital role in analyzing home investment loans, evaluating the risks and opportunities associated with these loans and providing guidance to borrowers and investors. By carefully considering the loan terms, LTV ratio, borrower’s creditworthiness, and financial situation, agents can help mitigate risks and maximize returns, making the real estate process a more secure and profitable experience for all.